Curious about which countries dominate the global economy today? Just as investors track the world’s biggest companies, understanding the greatest economies gives you a clearer picture of how global trade, innovation, and financial stability are shaped. According to the latest IMF World Economic Outlook (2025), the global economy is expected to reach nearly $117 trillion in nominal GDP. And as 2025 unfolds, several major players continue to influence everything from supply chains to financial markets.

In this article, you’ll find an easy-to-follow breakdown of the top 10 greatest economies in the world 2025, along with their GDP, growth outlook, inflation trends, unemployment rates, and key market highlights—helping you see how each country fits into the larger economic picture.

Greatest Economies in The World

Even in an ever-evolving landscape, a few trends remain constant. The United States continues to lead the world with its massive tech sector, high consumer spending, and deep financial markets. Meanwhile, China stays close behind, driven by manufacturing, exports, and an increasing shift toward domestic demand.

On the other hand, countries like India stand out due to strong economic momentum, while several advanced economies—including Japan and Germany—grapple with lower growth, inflation pressures, and shifting trade policies.

With that context, let’s explore the 2025 rankings.

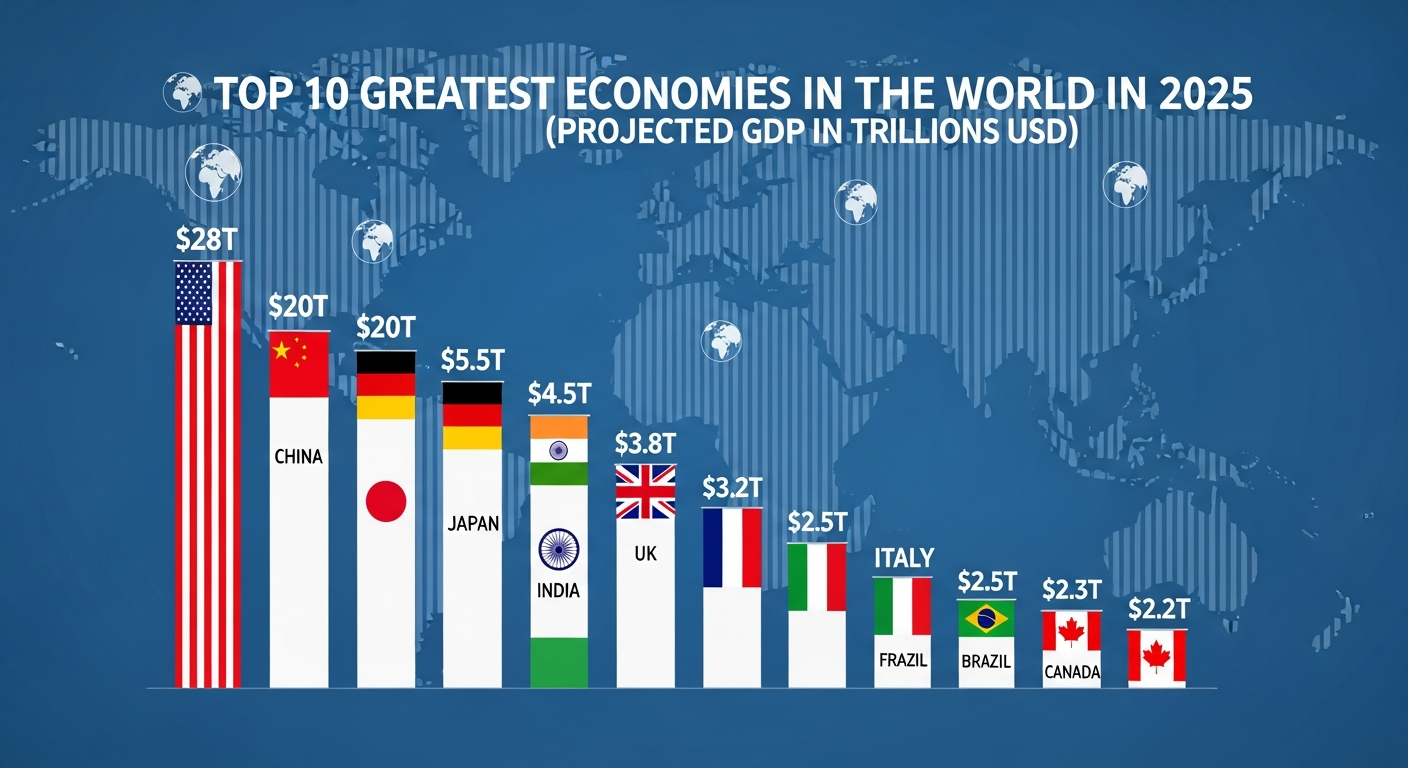

Top 10 Greatest World Economies (Nominal GDP)

| Rank | Country | Nominal GDP (USD Trillion) | Real GDP Growth (%) | GDP Per Capita (USD) |

|---|---|---|---|---|

| 1 | United States | 30.5–30.62 | 1.6–2.0 | 89,100–89,600 |

| 2 | China | 19.2–19.4 | 4.5–4.8 | 13,657–13,810 |

| 3 | Germany | 4.74–5.01 | 0.2 | 55,911–59,930 |

| 4 | India | 4.13–4.19 | 6.5–6.6 | 2,820–2,934 |

| 5 | Japan | 4.19–4.28 | 1.1 | 33,955–34,710 |

| 6 | United Kingdom | 3.84–3.96 | 1.3 | 54,949–56,600 |

| 7 | France | 3.21–3.36 | 0.7 | 46,792–48,980 |

| 8 | Italy | 2.42–2.54 | 0.5 | 41,091–43,160 |

| 9 | Canada | 2.23 | 1.2 | 53,558–54,930 |

| 10 | Brazil | 2.13 | 2.2 | 10,234 |

Other Economic Market Data

To give you a more complete picture, here’s how major economic indicators stack up across the world’s biggest economies:

| Rank | Country | Nominal GDP (USD Trillion) | Inflation (CPI %) | Unemployment (%) | Major Stock Index (YTD) |

|---|---|---|---|---|---|

| 1 | United States | 30.34 | 2.5 | 4.1 | S&P 500: +16.3% |

| 2 | China | 19.53 | 2.0 | 5.0 | Shanghai Composite: +12% (est.) |

| 3 | Germany | 4.74 | 2.2 | 5.5 | DAX: +18% |

| 4 | Japan | 4.21 | 2.0 | 2.6 | Nikkei 225: +10% |

| 5 | India | 4.11 | 4.5 | 7.5 | Nifty 50: +15% |

| 6 | United Kingdom | 3.58 | 2.3 | 4.4 | FTSE 100: +8% |

| 7 | France | 3.21 | 1.9 | 7.1 | CAC 40: +14% |

| 8 | Italy | 2.33 | 1.8 | 7.8 | FTSE MIB: +16% |

| 9 | Canada | 2.31 | 2.1 | 6.5 | TSX: +9% |

| 10 | Brazil | 2.31 | 4.0 | 7.2 | Bovespa: +11% |

United States — Still the World’s Largest Economy

The U.S. economy continues to lead the world in 2025, shaped by powerful forces across technology, healthcare, finance, real estate, and consumer spending. Much like how AI tools have transformed the way we work and create, America’s innovation-driven industries keep pushing the boundaries of what’s possible. With a GDP surpassing $30 trillion, the country’s strength comes from a dynamic tech sector, resilient consumer demand, and some of the deepest and most liquid financial markets on the planet.

Even though growth has settled into a mature, steady rhythm, the U.S. remains a global benchmark for productivity—especially as digital transformation and AI adoption accelerate. At the same time, the economy faces a few challenges, including rising tariff pressures that could add 0.5–1% to inflation and signs of a cooling labor market as job openings decline.

Still, the overall market environment remains strong. The S&P 500’s 16.3% year-to-date climb highlights just how influential megacap companies have become, with giants like Nvidia soaring more than 150%. While broader participation in the rally has softened, the U.S. maintains its position as the largest economy in the world, powered by consumption, investment, and a capital market structure known for its depth and flexibility.

China — Closing the Gap with Stabilizing Growth

China’s economic landscape is shifting—and fast. Long seen as the world’s factory floor, the country is now rewriting its playbook. Manufacturing still anchors its identity, but a surge in technology, services, and domestic consumption is redefining what drives growth. The result? China remains firmly in second place globally, with its economy edging toward $19.5 trillion and its influence on global supply chains still unmatched.

And much like how AI has reshaped the corporate leaderboard, China’s internal transformation is shaking up long-standing assumptions. The country is leaning harder into advanced manufacturing, electric vehicles, green energy, and high-tech innovation—sectors that are accelerating far quicker than earlier forecasts suggested.

Yet the momentum comes with friction. So, The property sector continues to drag on confidence, and U.S. tariffs—hitting key Chinese exports with rates as high as 25%—are testing the resilience of its growth model. Even so, infrastructure investment is roaring ahead, helping China outpace the U.S. in purchasing power parity (PPP) terms with an economic size above $39 trillion.

Financial markets are feeling the shift too. The Shanghai Composite is seeing a gradual rebound as policymakers pump in targeted stimulus and double down on future-focused industries like renewables and EVs. China’s rebalancing act—from export-led dynamo to consumption-driven powerhouse—is still underway, but the direction is unmistakable.

Japan — A Stability-Focused Advanced Economy

Japan’s economic story, much like a carefully crafted traditional dish, blends precision, heritage, and quiet resilience. Although the nation continues to face low growth and deep-rooted demographic challenges, it nevertheless preserves its position among the world’s leading economies. Its foundation rests on advanced manufacturing and cutting-edge technology—ingredients that have long shaped Japan’s global identity.

As we look deeper, the picture becomes more nuanced. On one hand, growth remains subdued, influenced by an aging population and persistent yen weakness. On the other, rising wages and a steady revival in tourism gradually add warmth to the country’s financial landscape. Moreover, the Bank of Japan has introduced a subtle but significant shift by raising interest rates to 0.5%, a move meant to steady inflation that has lingered stubbornly above target.

Meanwhile, the Nikkei’s impressive ascent can be traced to powerful export champions such as Toyota, whose global reach continues to anchor Japan’s industrial strength. However, much like a delicate recipe that depends on each ingredient being perfectly balanced, Japan’s outlook is still shaped by global trade tensions and supply-chain uncertainties.

At its core, the nation remains the world’s third-largest economy—an intricate mix of high-tech manufacturing, automobile innovation, and electronics production. It plays a vital role in global supply networks, contributing everything from precision components to robotics.

Ultimately, Japan moves forward in a low-growth environment where currency shifts and demographic realities play a defining role. Yet, despite these challenges, its mature financial markets, technological sophistication, and remarkably resilient export sector give the economy a character as enduring—and as carefully perfected—as one of its time-honored crafts.

Germany — Europe’s Economic Anchor

Germany’s position on the economic stage is shifting—yet it remains Europe’s undeniable heavyweight. While global dynamics are evolving, Germany still anchors the continent with an economy powered by world-class engineering, precision manufacturing, and a deep industrial backbone. And just as tech has reshaped global corporate rankings, Germany’s own economic landscape is undergoing a transformation of its own.

To begin with, the country continues to hold its title as Europe’s largest economy, supported by strong automotive, machinery, and chemical industries. However, rising energy costs and a slowdown in exports—especially to China—are reshaping the momentum. As a result, Germany’s growth outlook is more modest than in past decades, even as its innovation ecosystem keeps it firmly competitive on the world stage.

Moreover, this shift has had a noticeable impact on financial markets. The DAX has surged, fueled largely by increased defense spending and industrial leaders like Siemens climbing more than 25%. Although inflation has finally stabilized, Germany’s manufacturing PMI is still hovering just above contraction, signaling an industry in the middle of recalibration rather than acceleration.

At the same time, Germany is steadily transitioning toward sustainable energy and green manufacturing, a move that mirrors the global trend toward cleaner, more efficient production. This shift is not merely cosmetic—it is becoming a defining feature of Germany’s long-term strategy.

In essence, Germany remains the fourth-largest economy in the world, backed by advanced industry, machinery excellence, and a commitment to reinventing its energy and manufacturing systems. While the tempo of growth is subdued, the country is clearly navigating an industrial normalization phase—one that positions it for resilience amid a rapidly changing global economy.

India — The Fastest-Growing Major Economy

India, As country moves through another strong year, its growth is powered by energetic domestic demand, a flourishing services sector, and steady progress in manufacturing reforms.

Across the financial landscape, Foreign inflows are boosting confidence, the Nifty 50 is rising with notable strength in pharma and banking, and consumption remains firm despite the sharp lift in food prices. Each element adds its own character, creating a dynamic rhythm within the broader economy.

Looking ahead, India continues to stand out as one of the world’s fastest-growing major economies. With growth projected above 6.5%, the nation is steadily expanding its presence on the global stage. Its economy—now the fifth-largest—draws strength from a broad base: IT services, manufacturing initiatives like “Make in India,” and a massive consumer market that keeps activity flowing.

This momentum is supported by a market structure rooted in both services and manufacturing, backed by a deep pipeline of infrastructure development. As these sectors expand, they form the foundations of India’s long-term rise, reinforcing an outlook that remains upbeat for 2025 with growth estimated at 6.6%, followed by 6.2% in 2026.

With each passing year, India continues to build on its pace, shaping a growth story defined by scale, resilience, and an economy whose many moving parts work together with remarkable energy.

United Kingdom — A Services-Driven Powerhouse

The United Kingdom’s position in the global economy remains more resilient than headlines often suggest. While recent headwinds have tested its momentum, analysts note that the country continues to hold its ground thanks to the depth and diversity of its services sector. This foundation, combined with steady consumer spending, keeps the UK firmly in sixth place worldwide.

Yet, as several economists point out, the outlook is still shaped by lingering pressure points. Post-Brexit trade frictions continue to curb export efficiency, while housing inflation adds strain to households and borrowing costs—factors that collectively temper growth prospects. Even so, there are pockets of strength emerging. Services exports remain a bright spot, helping offset weaknesses in other segments of the economy.

Market performance reflects this mixed backdrop. The FTSE 100 has struggled to keep pace with global peers, largely due to volatility in the energy sector. However, banking stocks have shown surprising resilience; HSBC, for example, has climbed nearly 20%, signaling investor confidence in select financial names despite broader market caution.

Economists suggest that the UK’s overall pulse points to moderate growth ahead. Real-income gains are slowly improving spending capacity, and sectors tied to financial and professional services continue to act as stabilizing anchors. As long as wage recovery holds and inflation eases, demand is likely to stay supported—even in a challenging macro environment.

France — Balanced and Diversified

France’s position in the global economic rankings held steady as it maintained its status as the world’s seventh-largest economy, but sector-level pressures and policy adjustments shaped market sentiment through the week. Activity across its key industries—particularly aerospace, luxury goods, and services—showed a mixed performance, reflecting the country’s shifting competitiveness agenda.

Market watchers noted that growth remains moderate, with policymakers doubling down on investment-focused measures to support long-term momentum. However, pockets of softness emerged. Several firms tied to industrial supply chains traded lower as investors reacted to concerns about rising input costs and slower European demand. Meanwhile, services-linked stocks were comparatively stable, supported by consistent domestic consumption.

Despite these fluctuations, analysts emphasized that France’s broader economic framework remains intact. Its combination of industrial strength and a resilient services base continues to underpin stability, even as short-term market movements highlight the challenges ahead. Overall, sentiment suggests that while growth may stay measured, the country’s fiscal and competitive positioning keeps its long-term outlook on solid ground.

Italy — Slow but Steady Progress

When going to consider Italy’s economic landscape, Its growth remains softer than many of its European peers, yet there are gentle signs of improvement drifting in, supported by ongoing fiscal reforms and the broader umbrella of EU-backed frameworks. As the world’s eighth-largest economy, Italy moves through this cycle with a blend of caution and resilience.

Today’s Economic Outlook

The country begins its outlook with pockets of strength, particularly across its well-known manufacturing clusters—machinery, fashion, and specialty goods—much like early breaks of sunshine filtering through the clouds. Tourism, too, continues to bring a warm breeze of stability, especially in regions that rely heavily on seasonal activity.

However, the air is not entirely clear. Persistent regional disparities and high public debt—hovering around 140% of GDP—create a kind of economic humidity, keeping conditions slightly heavy and preventing sharper acceleration. These factors shape a macro pulse that stays closer to low growth, guided carefully by EU fiscal rules and Italy’s internal debt dynamics.

Market Conditions

In the markets, the FTSE MIB has shown brighter patches despite the broader sluggishness. Defense names such as Leonardo, up nearly 30%, act like strong sunbreaks, while renewable-energy stocks add pockets of brightness to the week’s market climate.

Overall Atmosphere

As Italy moves forward, the forecast suggests a continued mix of cloudiness and light improvement—a pattern where EU investments offer support, tourism softens pressures, and reforms gradually lift visibility. While the pace may remain gentle, the overall outlook carries hints of steadiness, much like a day that begins on a muted note but manages to hold its ground.

Canada — Resource-Rich and Labor-Strong

Canada’s economy in 2025 feels steady, gritty, and fuelled by a mix of raw resources and an ever-growing crowd of newcomers trying to make the whole thing louder and livelier. It isn’t flashy, it isn’t trying to be cool, but it holds its own in the global lineup as the ninth-largest economy, even if no one is throwing roses at it from the front row.

The country’s entire market structure has that familiar garage-band feel—rooted in old-school staples like oil and metals, while slowly layering in modern services like someone sneaking synths into a guitar-only jam session. Immigration keeps the labour force buzzing, like new bandmates showing up with fresh energy just when the old crew is burning out.

But, just like in those basement gigs where half the amps were broken, not everything hits the perfect note. Commodity exports keep the tempo going, but housing affordability issues and a dip in immigration are starting to throw off the rhythm, nudging unemployment upward. Still, the TSX is vibing to its own beat—commodity stocks, especially energy names, are up nearly 15%, strutting around like the local band that finally booked a decent festival slot thanks to a surge in global demand.

South Korea / Brazil — Competing for the Final Spot

Brazil and South Korea entered the global economic spotlight again this year, as new data placed both nations firmly in contention for the tenth position in the worldwide rankings. In Brazil’s case, the verdict was shaped by a familiar set of forces. The economy, carried by its vast reserves of natural resources, saw renewed momentum from agriculture, mining, and energy. Yet the stability of that rebound was questioned as fiscal deficits and ongoing currency volatility continued to weigh heavily on the country’s economic credibility. Markets reacted with intensity: the Bovespa’s climb echoed the strength of the commodity cycle, with Petrobras surging nearly 18%.

South Korea, meanwhile, delivered a performance driven by precision and power. The country’s advanced manufacturing engine—anchored in semiconductors, automobiles, and high-value exports—played a decisive role in lifting it into the global top tier. Analysts noted that the global tech cycle now acts as a critical swing factor for South Korea’s trajectory, capable of accelerating growth or stalling momentum with little warning.

In the final economic assessment, both nations were placed before the global scoreboard. Brazil stood as Latin America’s largest economy, rich in resources yet shadowed by structural challenges. South Korea, by contrast, was recognized for its disciplined manufacturing base and export competitiveness. Together, they formed the competing claimants to the world’s tenth-largest economy—each shaped by strengths that elevate them and vulnerabilities that threaten to pull them back.

Final Thoughts

Security-style monitoring of market conditions has also intensified as multiple risk factors come into focus, ranging from U.S. policy shifts to climate-related disruptions. Officials and analysts worldwide are keeping watch, aware that even a small shock could reverberate through markets and shave 0.5% off global GDP.

Key Economic Indicators Under Review

- Inflation Patterns:

Advanced economies are stabilizing near 2%–3%, while emerging markets such as Brazil and India show slightly higher yet steady inflation trends. - Stock Market Positioning:

The United States continues to dominate with the world’s largest exchanges (NYSE and NASDAQ). China follows closely, backed by the size of the Shanghai and Shenzhen exchanges. - Global Growth Outlook:

Growth is expected to soften to 3.2% in 2025, influenced by trade restrictions and geopolitical uncertainty. - Market Sentiment:

The MSCI World Index is up 10% YTD, with Europe outperforming the U.S. on the strength of defense and green-transition sectors, while emerging Asia leads in expansion potential. - Emerging Risks:

Analysts flag U.S. policy changes, rising conflicts, and climate events as immediate threats that could dampen global momentum.

Additional Data Options Available

- Core indicators: Nominal GDP rank, growth forecasts, and sector structure.

- Optional metrics: Equity index trends, sovereign bond yields, unemployment and inflation reports, FX movements, current-account balances, and sector breakdowns.

Leave a Reply