This page explains who qualifies for a home equity loan and how to find the best mortgage rates. Major U.S. banks commonly offer these loans with fixed rates, competitive terms, and broad availability. The guide compares APRs that include fees rather than just headline rates, and it covers prepayment penalties, HELOC draw-period and repayment terms, and closing costs. If you’re unsure, request quotes from multiple lenders or consult a mortgage broker to compare options efficiently. After reviewing this page you’ll have a clear plan for your home equity loan.

the U.S. home equity loan market was valued at approximately USD 175–180 billion in 2024, reflecting stabilization after rate hikes and steady demand. In 2025, the market is forecast at around USD 179–180 billion, with growth expected at about 4.3% CAGR through 2030, and HELOCs continuing to be a popular choice among borrowers.

This is for someone who do not know about what is an equity home loan.

Basically, An equity home loan is a secured loan backed by the value you’ve built in your property; you can borrow a lump sum or tap a revolving line of credit using your home as collateral.

Eligibility for Home Equity Mortgage Rates

Really equity mortgage rates is A fixed rate. this lump-sum second mortgage allows you to borrow against the equity in your home, providing the full amount upfront and requiring repayment through equal monthly installments over a term of 5 to 30 years.

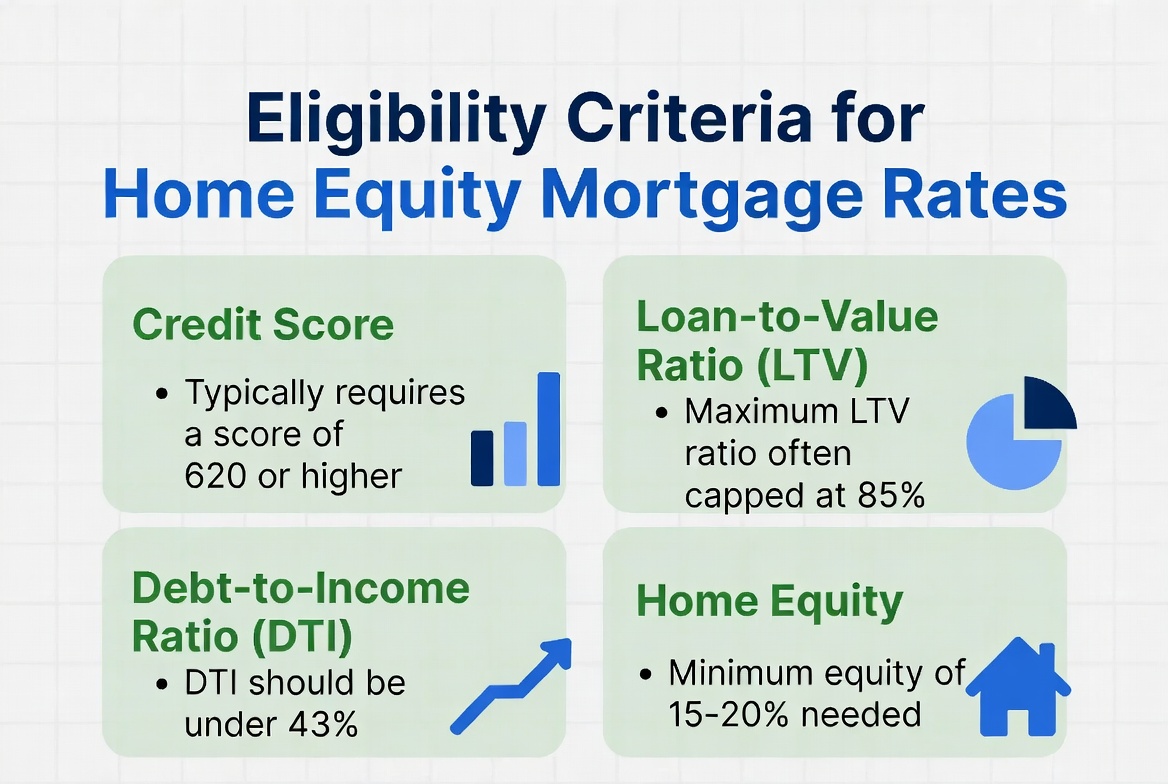

Before issuing this loan, most U.S. lenders assess key factors: the amount of equity in your property, your creditworthiness, your income and debt ratios, the property’s type and condition, and standard borrower documentation. Please read the article to know more details…

Eligible Property Types for Home Equity Loans in the USA

Beyond all other eligibility requirements, it’s essential to confirm whether your property type qualifies for a home equity loan. Without this key factor, any application attempt may be unsuccessful. If you’re considering an equity loan, review these details carefully: owner-occupied single-family homes and condominiums are the most commonly accepted collateral, while some lenders place restrictions on second homes, investment properties, or less conventional property types.

| Property Type | Generally Eligible? | Notes / Restrictions |

|---|---|---|

| Primary Residence (Single-Family Home) | Yes (Best terms) | Most commonly accepted by all lenders; best interest rates and highest LTV availability. |

| Condominium (Owner-Occupied) | Yes | Condo association/HOA must meet Fannie Mae/Freddie Mac or lender requirements; some lenders limit % of rental units. |

| Townhouse | Yes | Treated similar to single-family; must meet appraisal and title standards. |

| Second Home / Vacation Property | Yes (with conditions) | Higher interest rates and lower max LTV (typically 75–80%). |

| Rental / Investment Property | Sometimes | Stricter underwriting; lower LTV, higher rates. Only some lenders (TD Bank, Figure, Spring EQ, etc.) accept them. |

| Multi-Family (2–4 units) | Yes (with conditions) | Often must be owner-occupied (borrower lives in one unit). Investment-only deals have stricter rules. |

| Planned Unit Development (PUD) | Yes | Usually treated similar to single-family homes if project meets agency guidelines. |

| Manufactured / Mobile Homes | Limited | Must be permanently affixed and titled as real property. Typically only accepted if double-wide, built after June 1976, and on permanent foundation. Few lenders accept. |

| Modular Homes (permanently affixed) | Usually Yes | Must be on owned land and titled as real property. |

| Co-ops (Cooperative Units) | Almost Never | Many lenders restrict or refuse; mainly limited to specialty lenders in specific regions (e.g., New York). |

| Mixed-Use Properties | Very Limited | Often declined unless majority is residential and property meets strict guidelines. Usually only portfolio/specialty lenders. |

| Log Homes | Case-by-case | Must resemble conventional construction; some lenders accept. |

| Dome / Geodesic Homes | Rarely | Typically declined due to appraisal challenges. |

| Properties on Leased Land | No | Land must usually be owned; rare exceptions (e.g., some Hawaiian long-term leasehold properties). |

| Houseboats / Floating Homes | No | Not considered real estate. |

| Vacant Land / Raw Land / Lots | No | Home equity or mortgage financing not available without a permanent home structure. |

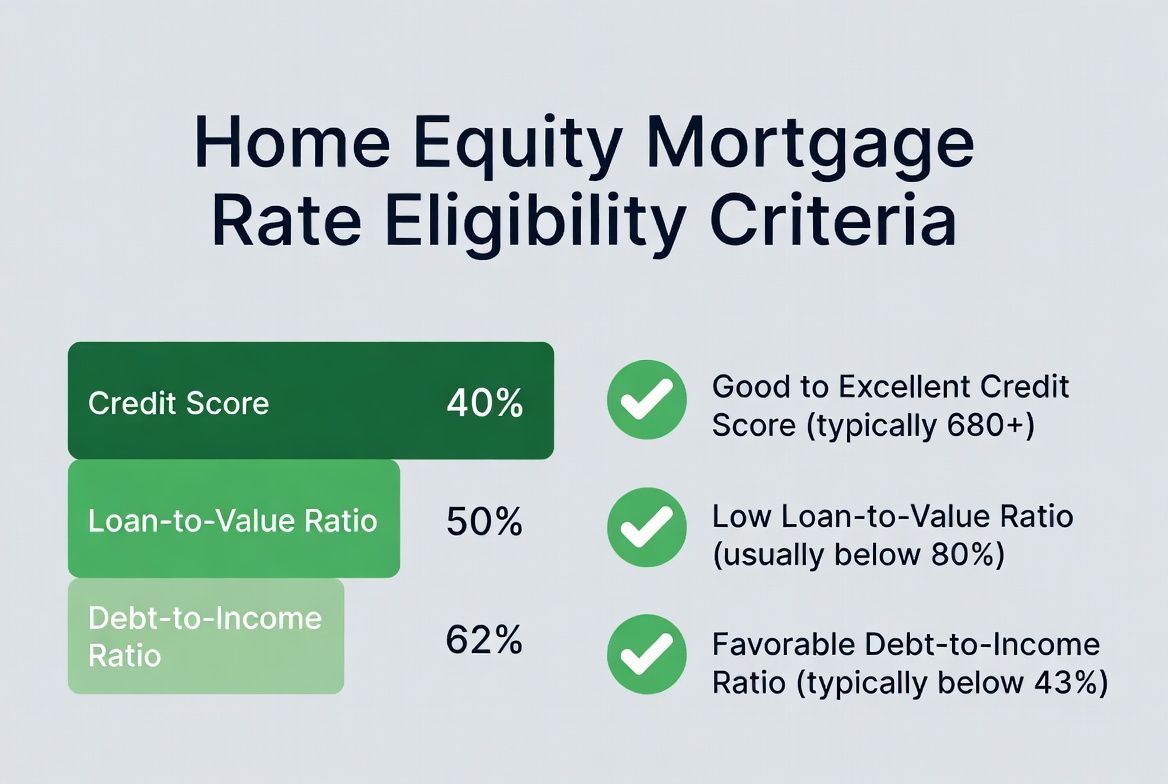

Equity Home Loan Eligibility Criteria

You might be wondering, “How much equity do I need to qualify?” The answer is straightforward: most lenders require you to maintain at least 15–20% equity after taking out the new loan, which translates to a combined loan-to-value (CLTV) ratio of 80–85%. In some cases, highly qualified borrowers may be approved with CLTVs as high as 90–95%.

When applying for a home equity loan, you’ll need to meet a minimum credit score requirement. Banks and financial institutions categorize borrowers by credit tiers. For instance, a score of 740 or higher typically qualifies you for the lowest advertised rates. A score of 620 is generally the minimum needed to obtain a mortgage loan from most lenders. If your score falls in the 680–700 range, you may still secure favorable rates.

as following topics, you will get more details about eligibility.

Top Banks Lists – Equity House Loan

Following lenders were chosen for strong performance in affordability, accessibility, and customer experience. Because rates and programs change frequently, it’s best to check lender websites directly or use comparison tools like LendingTree for tailored offers. If you live in certain states, local banks—such as Farmers Bank of Kansas City—may also provide strong home equity loan options.

| Bank / Lender | Features | Availability (States) | Min–Max Loan Amount | Terms (Years) |

|---|---|---|---|---|

| Rocket Mortgage | Online application; fast processing; HELOC + fixed-rate home equity options | Nationwide | $10,000 – $500,000+ | 5–30 |

| TD Bank | Low minimums; $99 origination fee; interest-only options; strong East Coast presence; up to 0.25% autopay discount; supports investment properties | 15 states + DC (primarily East Coast) | $10,000 – $500,000 | 5–30 |

| Third Federal / Third Federal Savings | Known for low rates; “lowest rate guarantee”; fixed & variable options; transparent fees; strong customer satisfaction | 18 states + DC (Midwest & East) | $5,000 – $300,000 | 5–30 |

| New American Funding | Higher LTV (up to ~90%); personalized service; competitive for mid-range loans | Nationwide | $25,000 – $500,000 | 5–30 |

| U.S. Bank | Low origination fees; HELOC with autopay discount (0.5%); online prequalification; strong customer support | 47 states (excluding TX, SC, DE) | $15,000 – $750,000 | 5–30 |

| PNC Bank | Fixed-rate and HELOC options; flexible underwriting; large loan options; may allow no appraisal | Nationwide (branches in 27 states) | $10,000 – $500,000 | 5–30 |

| Bank of America | No closing costs up to $1M; competitive promos; digital HELOC management; fixed-rate conversion | Nationwide | $15,000 – $1,000,000 | 5–30 |

| Wells Fargo | Flexible draw periods; large branch footprint; reliable national lender | Nationwide | $20,000 – $500,000 | 5–30 |

| BMO (Bank of Montreal) | No/low closing costs; 0.25% autopay discount; terms up to 20 years; wider reach after Bank of the West acquisition | Nationwide | $25,000 – $500,000 | 5–20 |

| M&T Bank | Intro rates from 5.99% for first 6 months; high borrowing limits; fixed or variable rate choices; good for second homes | 12 states + DC | $10,000 – $1,000,000 | 5–30 |

| Flagstar Bank | High maximum loan amounts; strong for large home projects; online application; part of NY Community Bancorp | Nationwide | $10,000 – $1,000,000 | 5–30 |

| Navy Federal Credit Union | No fees; competitive rates; strong for military and veterans; terms up to 20 years | Nationwide (membership required) | $10,000 – $500,000 | 5–20 |

| Discover | No origination fees; fast approval and funding; fully online; strong for debt consolidation | Nationwide | $35,000 – $300,000 | 5–30 |

Which lenders to consider

- Major national banks offer broad availability, solid customer support, and fixed-rate loan options.

- Regional banks and credit unions may provide lower fees, competitive rates, and more flexible underwriting.

- Online lenders are ideal for quick quotes, easy comparison shopping, and faster approvals.

- Mortgage brokers allow you to compare multiple lender offers through a single point of contact.

How to apply

1. Calculate how much equity you have and how much loan will sanction and interest rate

Start by estimating your home’s market value—either through online valuation tools or by getting a broker’s opinion. Then subtract your current mortgage balance to determine your available equity.

Lenders use a loan-to-value (LTV) limit to decide the maximum amount you can borrow.

How much can I borrow?

Common formula:

(Current home value × maximum LTV) − existing mortgage balance

Example:

$500,000 home × 85% LTV = $425,000

$425,000 − $200,000 remaining mortgage = $225,000 borrowing potential.

What is today’s average home equity mortgage rates? As of November 2025:

- Best rates: 7.00%–7.50% APR (excellent credit, LTV ≤ 60%)

- Average rates: 7.75%–8.75% APR

- Higher credit/LTV: 9%–11%+

2. Review credit, income, and debt-to-income ratio

Check your credit score and report—higher scores usually qualify for lower rates. Calculate your debt-to-income ratio (ideally 43% or less) and gather documents like recent pay stubs, W-2s, and tax returns to show stable income. Lenders verify all of these during underwriting to approve your loan and determine your interest rate.

3.Research loan types and lenders

Choose whether a fixed home equity loan (lump sum) or a HELOC (revolving credit line) fits your needs. Then compare interest rates, terms, fees, and minimum loan amounts from banks, credit unions, and online lenders.

4.Prequalify or get a soft preapproval

This type of loan is quick and convenient for customers to access. Many lenders offer prequalification tools that let you view potential loan amounts and rate ranges without affecting your credit score. These tools make it easier to compare offers, and also you can view their partnered with top-tier financial institutions, giving you the option to select the best fit before submitting a formal application.

5.Gather required documents

Most lenders request similar paperwork. Having everything ready up front can speed up approval to as little as 2–6 weeks.

- Identity & Personal Information

- Government-issued ID (driver’s license or passport)

- Social Security number or card

- Proof of residence if needed (utility bill, lease, etc.)

- Income Verification (recent 30–60 days + 2 years history)

- Recent pay stubs (usually 2–4)

- W-2 forms from the past 2 years

- Federal tax returns (1040s) for the last 2 years, including all schedules

- 1099s if applicable

- Self-employed applicants: 1099s, full business tax returns for 2 years, and current profit & loss statement

- Award letters for Social Security, pension, alimony, or other income sources

- Asset Statements (last 2–3 months)

- Bank statements for checking and savings (all pages)

- Statements for retirement or investment accounts (401k, IRA, brokerage, etc.)

- Current Mortgage & Property Information

- Latest mortgage statement

- Homeowners insurance declarations page

- Most recent property tax bill

- HOA dues or statements if applicable

- Additional Items (if required)

- Divorce or child support court orders

- Bankruptcy discharge records (if within the past 7–10 years)

- Gift letter if using gifted funds for reserves

Fastest Way to Submit

- Use the lender’s secure upload portal (e.g., Discover, Figure, U.S. Bank)

- Clear phone photos or PDF scans are acceptable, most of the bank allow you to sign a document through a e signature software they are using.

Pro Tip: Keep all documents in one digital folder before applying. With complete paperwork on day one, some lenders can issue approval in as little as 7–14 days.

After you submit documents

the lender orders an appraisal (usually $400–$800) to confirm your home’s current market value and calculate available equity. A title search is conducted to verify you own the property free of unexpected liens or disputes. Finally, underwriting begins: specialists thoroughly review your credit, income, DTI, appraisal report, title work, and all documents. They ensure everything meets guidelines and assess risk. Once approved, you receive a clear-to-close, schedule closing, and funds are disbursed (typically within 3–7 days). The entire appraisal-to-funding phase usually takes 10–30 days.

Closing, funding, Tax Deduction and Risk

Once approved, you’ll sign the closing documents, either in person or online depending on the lender. After closing, a home equity loan is paid out as a lump sum, while a HELOC gives you access to a revolving credit line you can draw from as needed.

Are there closing costs?

Yes. Most lenders charge about 2%–5% of the loan amount (roughly $2,000–$5,000 on a $100,000 loan). Common charges include appraisal fees, origination fees, title search, and recording fees. Some lenders offer “no closing cost” loans, where fees are absorbed in exchange for a slightly higher interest rate.

What are the risks?

- Your home is the collateral, so missed payments can lead to foreclosure.

- Monthly payments remain the same even if your home value declines.

- Borrowing too much can lead to financial strain and leave you “house poor.”

Is mortgage interest tax-deductible in 2025? if you are paying a ITR self-employed or salaried. Yes, this possible — but only when the loan proceeds are used to buy, build, or significantly improve the home that serves as collateral (see IRS Publication 936). Using the funds for debt consolidation or other non‑housing purposes is no longer deductible under current law. For personalized guidance, always confirm with a qualified tax professional.

Important loan features to check

this is your final consideration at the time of choosing a loan.

- Prepayment penalties: Some loans charge to pay early; confirm whether penalty applies and for how long.

- HELOC draw period and repayment: Understand length of draw period, whether interest-only payments are allowed, and how repayment works afterward.

- Rate floors and caps: For HELOCs, check rate floors and periodic/lifetime caps that limit how fast rates can increase.

- Lien position: Second mortgages or HELOCs add a lien that affects refinance or sale options. If you are willing to sell your house fast, check our page to get more details.

Leave a Reply